How Do Neobanks Make Money?

Neobanks are on a tear and users are loving them. Neobanks are online-only banks, typically funded by venture capital, that piggy-back on top of an existing institution’s banking license and offer a way for customers to store/spend money. Examples include Revolut, Nubank, Chime, Simple, N26, and more. They have a real shot at becoming the mainstream banking choice for customers over the next decade. Nubank, the most popular neobank in Brazil, recently announced that they have 15 million customers. For reference, Wells Fargo has 22 million active users on its mobile app. Neobanks are a rising force and key in understanding where the financial services industry is headed.

But how do these neobanks make money? The imprecise answer of “they make money when you swipe their card” doesn’t tell you much. In this post, I’ll concretely show how the mechanics of a neobank’s business model works.

Let’s take a look at Chime, the largest consumer neobank in the US. Chime’s core offering is a debit card alongside checking and savings accounts. They have nifty features like the ability to receive your paycheck two days early, no overdraft fees, and 100% mobile banking. With 60% of Americans not being able to cover a surprise $1,000 expense, a 2-day advance on a paycheck can be a huge relief for managing expenses. And the nixing of overdraft fees is a massive help for the US consumers paying a mind-boggling $34 billion/year in overdraft fees. These differentiated features have led to Chime amassing 5 million customers and $200 million in annualized revenue.

A neobank like Chime primarily makes money in two ways:

- Interchange revenue paid by payment processors (e.g., Stripe) when they process a payment for a Chime card

- Collecting interest from users’ deposits

Although some neobanks have different revenue streams (e.g., Wealthfront charges users roboadvisor fees as a percentage of the total value of assets stored with them), interchange and deposits interest are the two largest and most common revenue streams for neobanks. These are also some of the largest revenue streams for big banks (lending though typically being the largest).

Interchange

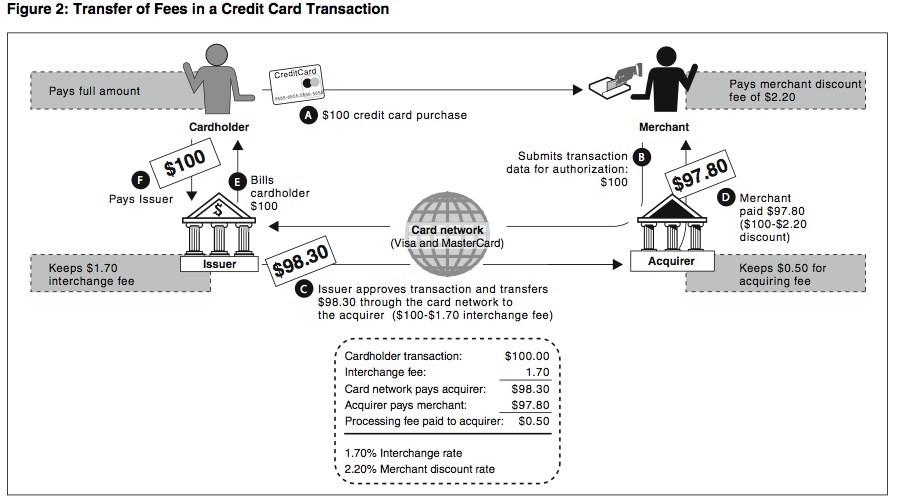

Interchange revenue is money that a card issuer (such as Chime) receives when someone swipes their card. Interchange is paid by the merchant through payment processing fees. The merchant is the party accepting a card payment in return for goods/services (e.g., your local supermarket). As an example, if a merchant uses Stripe for payment processing and is paying the standard 2.9% in transaction fees, Stripe will use a portion of that 2.9% to pay the card issuer.

An example breakdown of fees in a transaction

The specific amount paid to the card issuer depends on a number of factors and it varies for every transaction. The most important factors are:

- Whether the card is debit or credit

- Credit is significantly higher interchange

- Whether the card has specific rewards/perks

- Visa Infinite (many rewards/perks) has a higher interchange rate than the standard Visa card

- The type of the merchant for a given transaction

- Hotels have some of the highest interchange rates

Ultimately the card network (e.g., Visa) decides what the interchange rates are. The key equation for an interchange revenue stream is:

avg. interchange rate * total transaction volume

In Chime’s case, their cards are on the Visa network so Visa decides how much interchange they receive. The Visa interchange rates, along with Chime’s specific rates, are public 1. Depending on the type of merchant and transaction, Chime earns between 0.8% - 1.9% of a transaction’s amount, Although it’s impossible to know the exact amount of interchange Chime receives without knowing the distribution of Chime users’ spending, a reasonable guess based on aggregate consumer spending would put Chime’s average interchange rate at 1.25%2. This means that Chime receives around 1.25% of _all spending on their cards_. Not bad! There are still a handful of costs that Chime has to pay per transaction:

- Intermediary card processors

- Example: Chime uses Galileo, which likely charges them anywhere from 0.05% - 0.4% of transaction volume

- Fraud: if a customer loses their card and a thief spends money on it, Chime may have to cover the cost

- Note: keep in mind that since Chime is offering debit cards, not credit cards, there is no risk of the customer not paying back Chime for transactions

- Server costs: the server that has to process a transaction

Even with these costs, Chime is still making a handsome profit per transaction. Being the card issuer, as they are here, is a very high-margin business.

Deposits Interest

Interest revenue is earned by a depository institution investing customer funds in low-risk securities. The depository institution typically also pays the customer for keeping their deposits at the institution. The key equation for profitability of this revenue stream is:

(% interest earned - % interest paid to depositor) * deposits amount

The % interest earned for neobanks is typically equal to the effective federal funds rate. Because the federal funds rate is constantly shifting, the profitability of this revenue stream for neobanks is constantly shifting. This is why neobanks frequently change the interest rate offered to depositors (see Wealthfront’s blog as an example). This is a stark contrast to big banks however. A key benefit of a banking charter is that banks can lend out a multiple of their deposits as loans (e.g., mortgages, business loans). This amount is referred to as net interest margin, and is typically much higher than the federal funds rate - it was 3.3% on average for banks in 2018. The _% interest paid to depositor* is how much the depositor earns by storing their funds with the institution, and is set by the depository institution. For the recent wave of high-yield accounts offered by neobanks, they’ve set % interest paid to depositor essentially equal to *% interest earned_, making this revenue stream’s profitability close to zero. The typical rationale is for the high-yield account to draw in consumers for other higher-margin products such as debit/credit cards or loans.

In Chime’s case, % interest earned (the federal funds rate) is 0.09% at the time of writing (Sept. 2020), and % interest paid to depositor is 1.00%. This means that Chime is actually losing money on their deposit account product, and likely using it as a loss leader for the debit card, which has far higher profit margins. Also note that Chime only gives depositors 1% in interest for funds in their savings account. For any funds in the checking account (which over all customers may be larger), no interest is given.

These are the two main revenue streams for the majority of neobanks, but there are also others such as cross-selling, reward redemption referrals, and new ones being created by startups. Hopefully this has given you a grasp of the basics, let me know if you have any thoughts/questions below!

-

Chime’s interchange rates are listed in Section A, under the column “Exempt Regulation”. ↩

-

Derived from 2019 Federal Reserve Payments Study and U.S. Bureau of Labor Statistics Annual Consumer Expenditure Report ↩